In federal accounting, an obligation is when you have a legal requirement to pay an amount of money for goods or services. Obligations occur after funds have been committed. This matters because once funds are obligated, your agency can then receive goods or services and pay for them. Federal agencies track obligations using four main USSGL accounts, depending on delivery and payment status.

Official Definition

According to the GAO's Federal Budget Glossary, an Obligation is defined as:

“A definite commitment that creates a legal liability of the government for the payment

of goods and services ordered or received, or a legal duty on the part of the United

States that could mature into a legal liability by virtue of actions on the part of the

other party beyond the control of the United States. Payment may be made

immediately or in the future.”

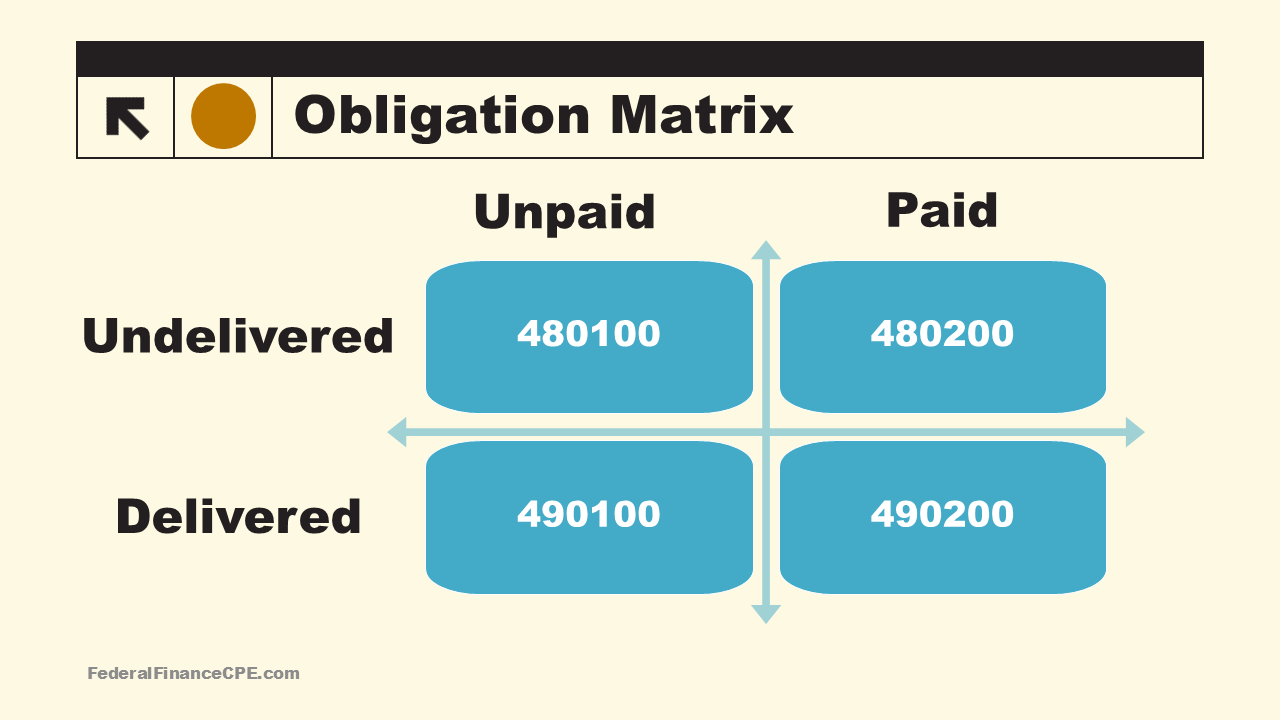

This account is used to record the amount of goods and/or services ordered, which have not been actually or constructively received and for which

amounts have not been prepaid or advanced. This includes amounts specified

in other contracts or agreements such as grants, program subsidies,

undisbursed loans and claims, and similar events for which an advance or

prepayment has not occurred. This account does not close at year-end.

Although the normal balance for this account is credit, it is acceptable in

certain instances for this account to have a debit balance.

This account is used to record the amount of goods and/or services ordered,

which have not been actually or constructively received but have been

prepaid or advanced. This includes amounts specified in other contracts or

agreements such as grants, program subsidies, undisbursed loans and claims,

and similar events for which an advance or prepayment has occurred. This

account does not close at year-end.

490100 - Delivered Orders, Unpaid

This account is used to record the amount accrued or due for: (1) services

performed by employees, contractors, vendors, carriers, grantees, lessors,

and other government funds; (2) goods and tangible property received; and

(3) programs for which no current service performance is required such as

annuities, insurance claims, benefit payments, loans, etc. This account does

not close at year-end. Although the normal balance for this account is credit,

it is acceptable in certain instances for this account to have a debit balance.

490200 - Delivered Orders, Paid

This account is used to record the amount paid/outlayed for: (1) services

performed by employees, contractors, vendors, carriers, grantees, lessors,

and other government funds; (2) goods and tangible property received; and

(3) programs for which no current service performance is required such as

annuities, insurance claims, benefit payment, loans, etc.

What This Means in Practice

In day-to-day federal work, Obligations usually come up when budgeting for the next year, planning acquisitions, and monitoring undelivered orders. You also want always to be sure you do not "spend" more than what was obligated, or that might be an Anti-Deficiency Act violation.

Simple Example

Here’s a straightforward example:

Your agency committed $10,000 for laptops. Your Contract officer signed a contract for $10,000 worth of laptops. When this happens, you move your budgetary resources from 470000 to 480100.

Common Mistakes or Confusion

Assuming that once funds are obligated, no further monitoring is needed to verify that they are still required. If a project ends with funds still obligated, you need to de-obligate those funds, as they no longer meet the definition of an obligation, as there would be no liability to pay.

Where You’ll See This Term Used

You’ll commonly see Obligations in:

Statement of Budgetary Resources

SF 133 Report on Budget Execution and Budgetary Resources

OMB Circular No. A-11

Undelivered Order Monitoring

Want to go deeper?

This term is covered in our federal accounting CPE course on Budgetary Accounting.